Created a tick db:

from quantrocket.realtime import create_ibkr_tick_db

create_ibkr_tick_db("ibkr-fx-eurusd-1min-tick", universes=["ibkr-fx-eurusd-1min"],

fields=["LastPrice", "Volume", "BidPrice",

"AskPrice", "BidSize", "AskSize"])

Created an realtime aggregate db:

from quantrocket.realtime import create_agg_db

create_agg_db("ibkr-fx-eurusd-1min",

tick_db_code="ibkr-fx-eurusd-1min-tick",

bar_size="5m",

fields={"LastPrice":["Open","High","Low","Close"], "Volume": ["Close"]})

List dbs:

from quantrocket.realtime import list_databases

list_databases()

{'ibkr-fx-eurusd-1min-tick': ['ibkr-fx-eurusd-1min']}

Check db config for aggregate db:

from quantrocket.realtime import get_db_config

get_db_config("ibkr-fx-eurusd-1min")

{'tick_db_code': 'ibkr-fx-eurusd-1min-tick', 'bar_size': '5m', 'fields': ['LastPriceClose', 'LastPriceHigh', 'LastPriceLow', 'LastPriceOpen', 'VolumeClose']}

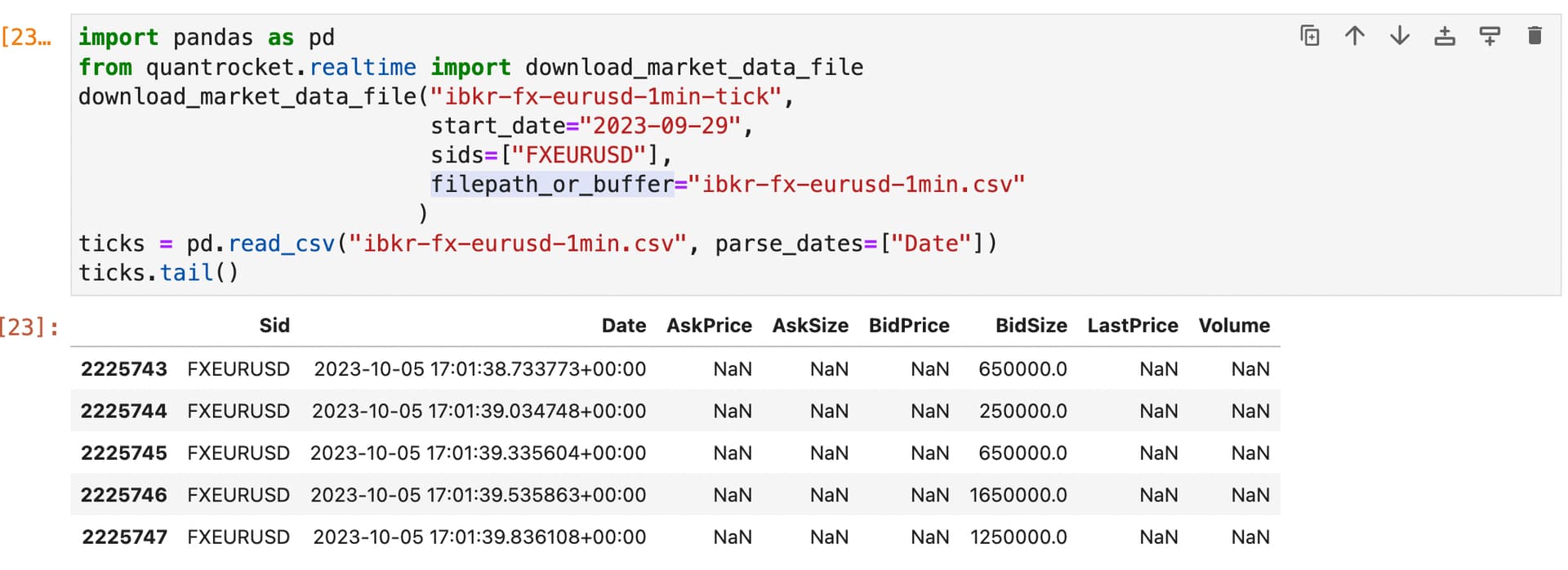

Fails to query realtime aggregate db:

download_market_data_file("ibkr-fx-eurusd-1min",

start_date="2023-09-29",

sids=["FXEURUSD"],

fields=['LastPriceClose',

'LastPriceHigh',

'LastPriceLow',

'LastPriceOpen',

'VolumeClose'],

filepath_or_buffer="ibkr-fx-eurusd-1min.csv"

)

NoRealtimeData: ('400 Client Error: BAD REQUEST for url: http://houston/realtime/ibkr-fx-eurusd-1min.csv?start_date=2023-09-29&sids=FXEURUSD', {'status': 'error', 'msg': 'no market data matches the query parameters'})

Can you help me investigate this?