Hi there,

In this backtest, I have a function that's scheduled to execute trades at 1 hour and 2 hours after the market opens:

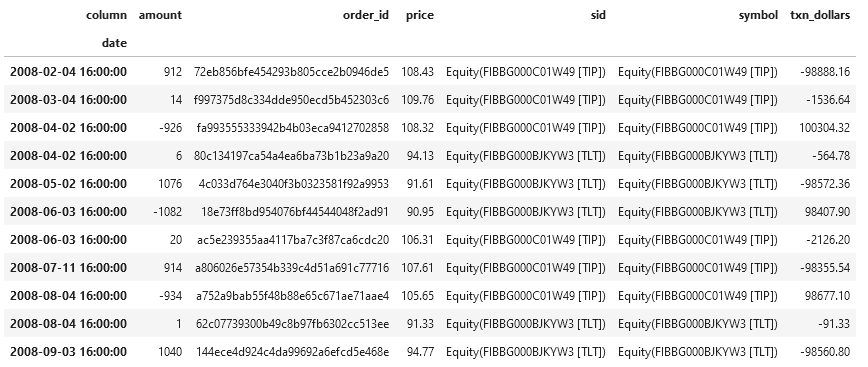

However, when I view the transactions, it looks like all of them are executing right at the market close:

Since the strategy only re-balances monthly, it looks like parts of the trade are being pushed into the following month which is having a negative impact on the returns.

Is there anything I need to do to make sure the backtest algorithm executes the entire trade at the designated time? Also, is the pushing of the new buy orders due to cash settlement timing as the buy orders are effectively using all of the cash allocated to the strategy that only becomes available when a sell executes?

David