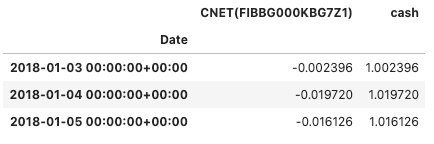

Noticed cash positions being greater than 1.0 within backtest results from a short only strategy, and thought this might be a bug, but wanted to confirm.

In pyfolio/quantrocket_moonshot.py the from_moonshot method returns the following for positions:

I would think cash would be 1 - active positions, which appears to be the intention within from_moonshot per the following code snippet:

returns = results.loc["Return"].sum(axis=1)

positions = results.loc["NetExposure"]

positions["cash"] = 1 - positions.sum(axis=1)

Should the last line maybe use abs() before sum() instead?

positions["cash"] = 1 - positions.abs().sum(axis=1)